Are you tired of feeling the stress of debt? Do you dream of a life free from financial worries? This article provides practical, actionable steps to help you make everyday decisions that will significantly impact your financial well-being and keep you out of debt. Learn proven strategies for budgeting, saving, and spending wisely, ultimately achieving financial freedom and peace of mind. Discover how small, consistent choices can lead to big changes in your overall financial health.

Understand Your Spending Triggers First

Before you can effectively manage your finances and stay out of debt, it’s crucial to understand your spending triggers. These are the situations, emotions, or thoughts that lead to impulsive or unnecessary purchases. Identifying these triggers is the first step towards breaking the cycle of overspending.

Common triggers include stress, boredom, emotional distress, social pressure, or even simple convenience. Consider keeping a spending journal to track your purchases and note the circumstances surrounding them. This will help you pinpoint patterns and recognize your personal spending triggers.

Once you’ve identified your triggers, you can develop strategies to manage them. This might involve practicing mindfulness before making a purchase, finding alternative ways to cope with stress (like exercise or meditation), or setting a cooling-off period before making a non-essential purchase. Learning to recognize and manage these triggers is a powerful tool in your journey towards financial freedom.

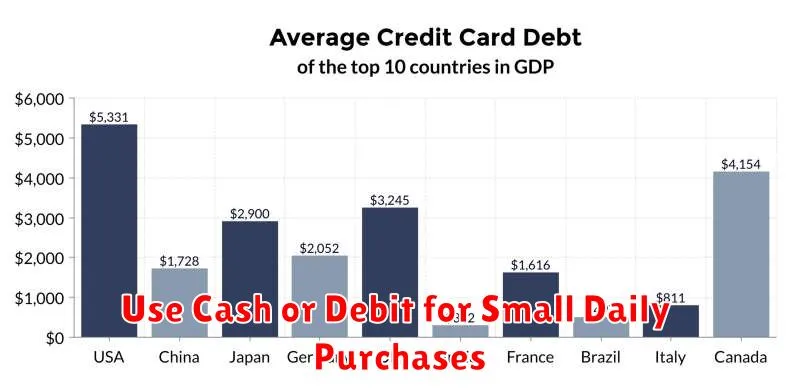

Use Cash or Debit for Small Daily Purchases

Small, everyday purchases can significantly contribute to debt accumulation over time. Avoid using credit cards for these transactions. The interest charges, even on small balances, quickly add up.

Instead, utilize cash or debit cards. Cash provides a tangible limit to your spending, forcing mindful budgeting. Debit cards directly deduct funds from your checking account, preventing the buildup of credit card debt.

Careful tracking of these small expenses, whether via a notebook or budgeting app, will further enhance your awareness of your spending habits and help you stay within your budget.

By consistently using cash or debit for daily purchases, you’ll gain better control of your finances and significantly reduce your risk of accumulating unnecessary debt.

Keep a Strict Limit on Credit Card Use

Credit cards can be convenient, but they are a major source of debt for many. To avoid accumulating debt, establish and strictly adhere to a spending limit on your credit cards. This means setting a budget and only charging expenses you can comfortably afford to repay in full each month.

Avoid using credit cards for non-essential purchases. Prioritize paying off your existing balance before making additional charges. Track your spending meticulously to ensure you remain within your self-imposed limit. Consider using cash or debit cards for everyday purchases to help control impulsive spending.

Regularly review your credit card statements to identify areas where you can cut back. High interest rates can quickly lead to significant debt, so minimizing credit card use is crucial for long-term financial health. Paying down your balance as quickly as possible is key to staying out of debt.

Setting a strict limit and consciously using credit cards only for planned and affordable expenses is vital. This disciplined approach significantly reduces the risk of falling into unsustainable debt.

Make a Rule Before You Buy Anything Over $100

Implementing a pre-purchase rule for items exceeding $100 is a crucial step in effective debt management. This involves establishing a defined waiting period—ideally, 24 to 72 hours—before finalizing any purchase above this threshold. This delay allows for rational consideration of the purchase’s necessity and value, preventing impulsive spending.

During this waiting period, critically evaluate the item’s true value against your existing budget and financial goals. Ask yourself: Is this purchase essential? Can I afford it without jeopardizing other financial obligations? Are there cheaper alternatives? This thoughtful process significantly reduces the likelihood of acquiring unnecessary debt.

Beyond the waiting period, consider exploring alternative financing options if the purchase remains necessary. Instead of relying on high-interest credit cards, explore lower-interest loans or saving up for the item entirely. This approach fosters responsible spending habits and safeguards your financial stability.

Build Emergency Savings to Avoid Borrowing

Building an emergency savings fund is crucial for avoiding debt. Unexpected expenses, like car repairs or medical bills, can quickly derail your finances if you don’t have a safety net. Aim to save 3-6 months’ worth of living expenses in a readily accessible account.

Regular contributions, even small amounts, are key. Automate transfers from your checking account to your savings account to make saving effortless. Consider setting a realistic savings goal and tracking your progress to stay motivated.

Having an emergency fund allows you to handle unexpected costs without resorting to high-interest debt such as credit cards or payday loans. This prevents the accumulation of debt and its associated interest charges, significantly improving your long-term financial health.

Say No to Things You Can’t Afford Now

One of the most crucial steps to avoiding debt is learning to say no to purchases you cannot currently afford. This seemingly simple act prevents the accumulation of credit card debt and high-interest loans.

Before making any purchase, ask yourself: Can I comfortably afford this without impacting my budget or requiring me to borrow money? If the answer is no, postpone the purchase. Consider saving for the item instead. This allows you to buy it outright, avoiding the added costs associated with financing.

This strategy fosters a mindset of financial responsibility and helps you prioritize your spending based on your actual financial capacity. It empowers you to make informed decisions, preventing impulsive buying that often leads to debt.

Remember, delaying gratification for something you can’t afford now is a powerful tool in building a strong financial future. It allows you to achieve your financial goals faster and with less stress.

Celebrate Living Debt-Free

Achieving a debt-free life is a significant accomplishment, deserving of celebration. It represents financial freedom and opens doors to new possibilities. Take the time to acknowledge this milestone; you’ve worked hard to reach this point.

Consider how you’ll mark this achievement. A small, meaningful celebration can reinforce your commitment to responsible financial management. This could be anything from a quiet night in with loved ones to a small purchase you’ve been saving for. The key is to celebrate your success without incurring new debt.

More importantly, use this moment as an opportunity to solidify your long-term financial health. Review your budget, reaffirm your savings goals, and plan for the future, ensuring you maintain your debt-free status. This celebration is not just about the past, but about securing a brighter, more financially stable future.

Remember, staying debt-free requires consistent effort and mindful decision-making. By celebrating your achievements, you reinforce positive financial habits and stay motivated to continue on your path towards financial well-being.

{kind=link}